I’ve been a Bank of America (BofA) customer ever since my parents helped me open my first account when I was a child (and I’m still a happy customer today).

Naturally, I wasn’t thinking about lifecycle back then. But now, as a marketer, I’ve got a whole new lens I look at companies through. I got really curious about what strategies one of the largest financial institutions uses to keep customers coming back. So I decided to analyze every message they sent me in 2025 (135 emails to be exact).

What I found was a masterclass in cross-selling. Most brands treat transactional emails (receipts, statements, alerts) as an afterthought. Bank of America treats them as the primary engine to power their multi-product flywheel.

Here is the exact strategy they use to anchor their brand to life's most important moments, driving users to other products in their ecosystem. And it’s one that any company can learn from, whether or not you’re in fintech.

The retention problem

In banking, the product isn’t the checking account; the product is the relationship. Fintech is a commodity game. If you only have a checking account, you are one "sign-up bonus" away from switching to a competitor.

More often than not, the best indicator of retention, loyalty, and LTV is product density: the number of integrated products a customer uses, from checking and savings accounts to credit cards to mortgages, retirement accounts, and more. And though the mix of offers may be different at every company, thinking about product density is often one of the most important north stars marketers can anchor toward.

The core strategy: “inertia engineering”

To solve this "commodity trap," BofA uses what I call “inertia engineering.” In marketing, inertia is usually the enemy—it’s the "low-activity" state where customers ignore your emails because they have no reason to engage. BofA flips this by engineering moments of action into the only things customers already have the momentum to do: checking their balance or opening a statement.

Subject line: Your statement is available

They leverage the high-trust attention and engagement of account statement messages to anchor their entire lifecycle strategy.

Their program’s single aim? Helping you solve for life's biggest friction moments before you even realize you're in them. The entire lifecycle program hinges on these sends because transactional emails guarantee engagement, and engagement primes the inbox for cross-sell opportunities to drive product density. They leverage everything they know about you to move from reactive banking to proactively helping you solve complex financial problems, and for BofA, that manifests in five core cross-sell use cases.

The 5% intercept strategy

There’s a famous stat that goes something like this: Only 5% of your customers are ready to buy at any given point in time. The real challenge for any lifecycle team is figuring out what to do with the other 95% of the time when they aren't in a "buying window." Most lifecycle teams treat transactional (system-generated) and promotional (marketing-generated) emails as two different worlds.

Most brands ignore the 95% until they "raise their hand." BofA does the opposite. They use transactional shadowing to bridge the gap between "just checking my balance" and "needing a new product."

By sequencing marketing sends to arrive in the wake of your most important account alerts, BofA ensures their offers don't feel like random "batch and blast" noise. Instead, they feel like a logical next step. For the 95%, this builds the "financial co-pilot" brand. For the 5%, it intercepts them at the perfect time in their next major financial decision.

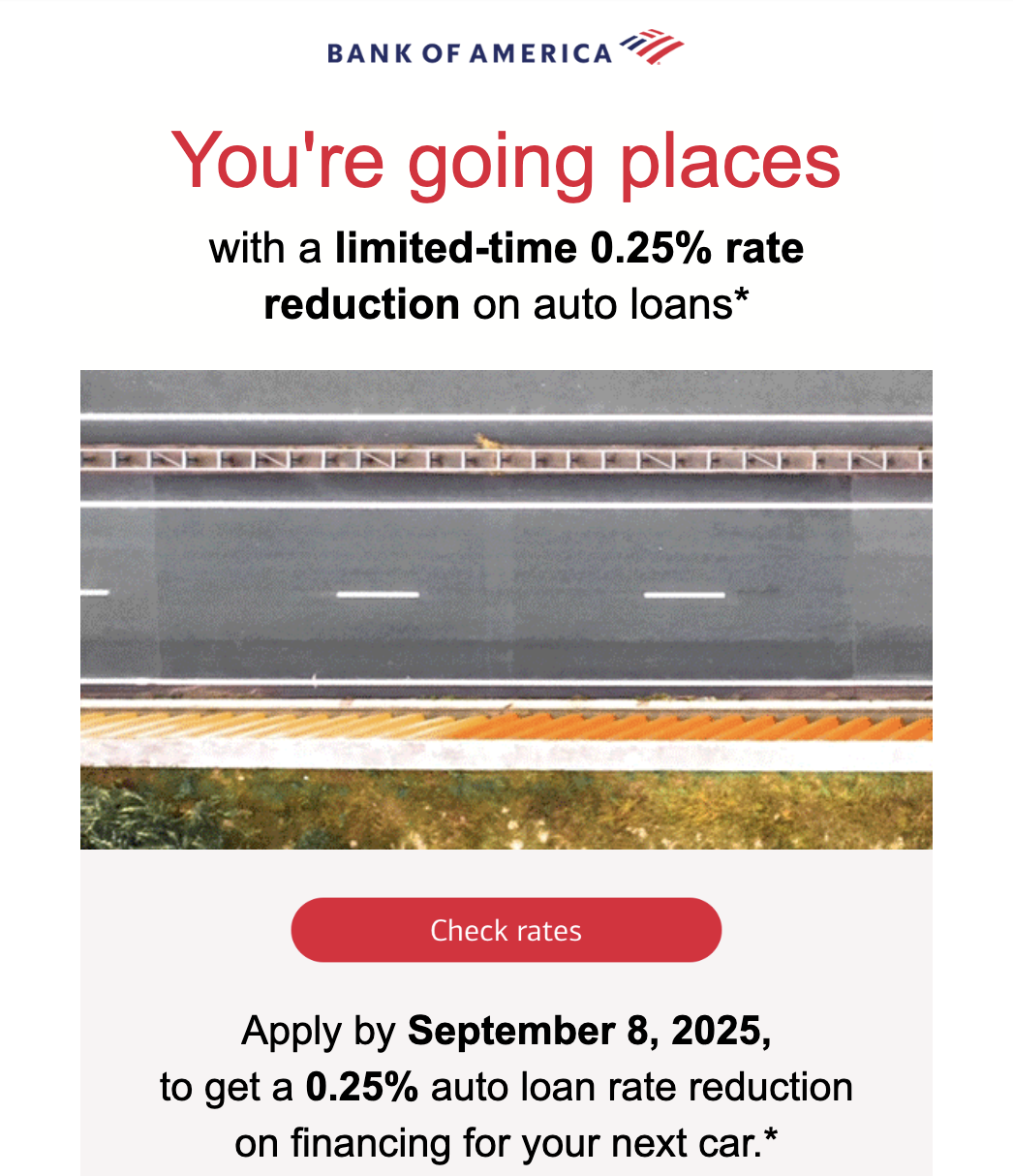

Here are the five core intercepts they’re running to drive product density:

|

||

|

||

|

||

|

||

|

The lesson: don’t waste your transactional emails

The real genius behind BofA’s lifecycle program is that they never waste a transactional email because they are the backbone of the entire marketing engine. But even more than that, they’re also a retraining tool. One thing that I didn’t really cover which is really interesting is that in every single bank statement there’s a subtle nudge to use BofA’s AI assistant: Erica. And in an AI world that’s huge because they’re slowly retraining every customer to redirect requests to their AI. This is key for two reasons:

Operational efficiency: Erica can offload simpler requests away from the actual support team so they can focus their time and efforts on interactions that can only be resolved with a human.

Better personalization: Every interaction with Erica helps BofA better understand customer intent, which then fuels every personalized experience.

And all of this once again ties back to the overarching theme of delivering more customer value because the better you understand the customer, the faster you can eliminate friction and the faster you can solve their problems.

The 99% retention secret

There’s a reason their Preferred Rewards program has a 99% retention rate. You don’t stay with BofA because you're "trapped" by a checking account; you stay because you don't want to lose the financial co-pilot that is already three steps ahead of your next big life moment.

I saw this in action when I received a perfectly timed auto-loan offer just as I was entering a car-buying window. And if you know how to read the "receipts" in the campaign parameters, you can see it wasn't a coincidence:

`https://promotions.bankofamerica.com/autoloans/nextgen?ep=empty&mktgCode=EmFeb26d1pur206&cm_mmc=eLend-Auto-_-email-_-EA24EM00T1_check_rates_cta_top-_-06654_purch_relax_ls`BofA isn’t just a bank that manages money; they're trying to make life easier through the "boring" stuff.

One more thing…

I’ve heard how valuable these breakdowns are for our community, and now I’m even more curious to dive into fintech. So if you work at a financial services company and want to see your lifecycle program broken down like Bank of America, shoot me an email directly at [email protected], and I’ll do a free audit and workshop with you.